If you're considering a career in accounting, there are several options to choose from. There are several options. You could work for a large firm, one or more of the "Big Four" accountants, or start your own firm. These are just a few of the advantages and disadvantages of each route. Which one would suit you best? Which one will have the greatest impact on your salary? Which career path will get you a better salary? And what kind of experience will be necessary to succeed?

You can only work for one company

A single accounting company might not be the right fit for you if you're looking to pursue a career in accounting. People tend to stay in an entry-level position for one to five years. This is dependent on the organization, economy and opportunities elsewhere. This article assumes that you will remain at the same company for one year. Final decision is up to you.

The ability to earn a high salary

If you are a math whiz and love to work with numbers, an accounting career might be for you. Accounting is a popular career option because it pays a median salary of $92,246, which is a high average. As the head of an accounting department, you'll oversee all aspects of a company's finances. These include financial statements and general ledgers, payroll, accounts payable, receivable and tax compliance. You will also need to manage budgeting and tax compliance.

Some accountants work in large firms as CFOs, or in small firms as partners. Others work for clients, filling out tax returns on their own. High salaries are available in accounting careers, so it's possible to work remotely. It just requires a bit of creativity and determination. But if you're determined, you'll find a high-paying accounting job that doesn't require a big commute or much travel.

Work for one of the "Big Four" accounting firms

Many people dream about working at one of the Big Four accounting firms. But, what are the drawbacks and benefits? If you're looking for an entry-level accounting position, there are many reasons to work for a Big Four firm. These are the benefits and drawbacks of working for a Big Four or regional firm. You will then be able to decide if this role is right for yourself.

When applying to a Big Four firm, be sure to demonstrate the qualities that make a good employee for the company. You should be confident and determined to serve the clients and company. Your ability to show your commitment to the vision of the company, to be financially savvy and to have emotional intelligence are also important. These attributes are not enough. You also need to be able to use computers and understand tax and accounting laws.

Start your own accounting business

There are some key points to remember when starting an accounting business. There are many benefits to owning your own accounting firm. However, you need to be ready to invest some time researching. It is important to understand what you are legally allowed to offer your clients. For example, only a CPA is allowed to file reports with SEC. It can be difficult to find clients due to this.

Entrepreneurship can combine your accounting skills with your entrepreneurial spirit. In addition to having the support of your family and a flexible schedule, you can also establish a successful business from home. While you might not have full control over your business' strategic direction, you have the freedom to do what you enjoy most. A small business can thrive without a large team of accountants. You should think about how your skills could benefit your clients.

FAQ

What kind of training is necessary to become a bookkeeper?

Basic math skills are required for bookkeepers. These include addition, subtraction and multiplication, divisions, fractions, percentages and simple algebra.

They also need to know how to use a computer.

The majority of bookkeepers have a high-school diploma. Some even have college degrees.

What does it mean to reconcile accounts?

The process of reconciliation involves comparing two sets. One set is called the "source," and the other is called the "reconciled."

The source is made up of actual figures. The reconciliation represents the figure that should actually be used.

If you are owed $100 by someone, but receive $50 in return, you can reconcile it by subtracting $50 off $100.

This process ensures that there aren't any errors in the accounting system.

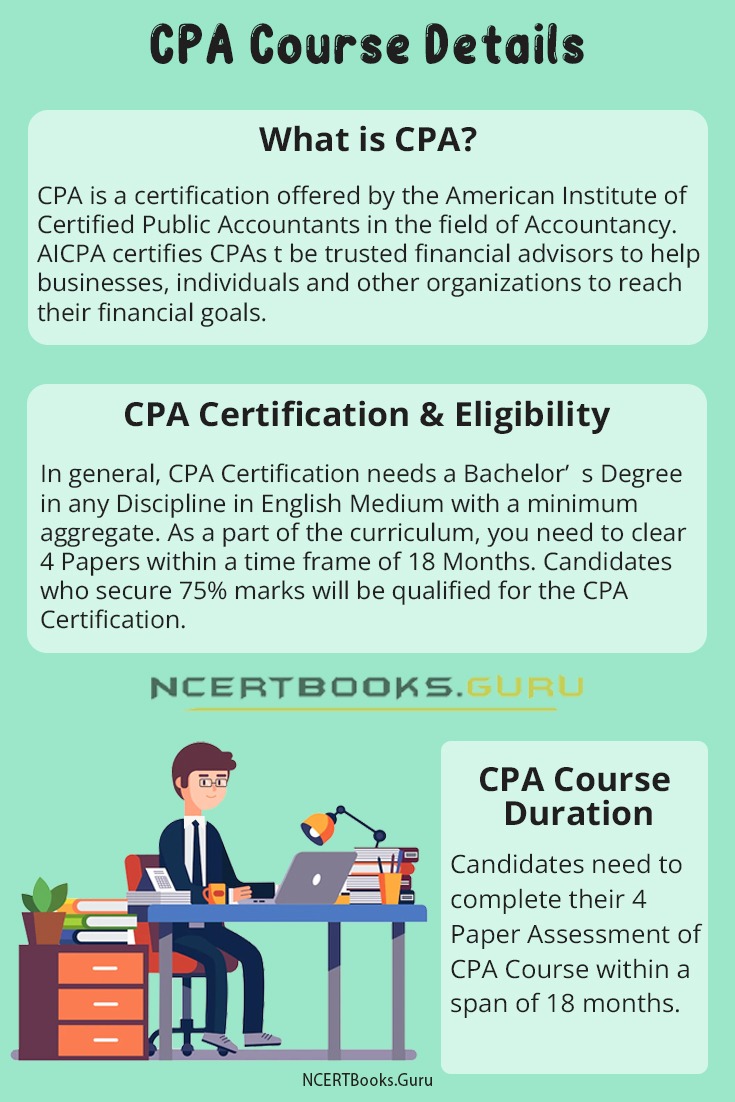

What is the average time it takes to become an accountant

The CPA exam is necessary to become an accountant. The average person who wants to become an accountant studies for approximately 4 years before sitting for the exam.

After passing the exam, one must be an associate for at most 3 years in order to become a certified public accounting (CPA) after passing it.

What is the difference in Chartered Accountant and a CPA?

Chartered accountants are accountants who have passed all the necessary exams to get the designation. Chartered accountants have more experience than CPAs.

Chartered accountants are also qualified in tax matters.

The average time to complete a chartered accountancy program is 6-8 years.

What is the difference between accounting and bookkeeping?

Accounting is the study of financial transactions. Bookkeeping is the recording of those transactions.

The two are related but separate activities.

Accounting deals primarily with numbers, while bookkeeping deals primarily with people.

Bookkeepers record financial information for purposes of reporting on the financial condition of an organization.

They ensure all books balance by correcting entries in accounts payable and accounts receivable.

Accountants examine financial statements in order to determine whether they conform with generally accepted accounting practices (GAAP).

If they are unsure, they might recommend changes in GAAP.

Bookskeepers record financial transactions in order to allow accountants to analyze it.

Statistics

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- Employment of accountants and auditors is projected to grow four percent through 2029, according to the BLS—a rate of growth that is about average for all occupations nationwide.1 (rasmussen.edu)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

External Links

How To

Accounting for Small Business

Accounting for small businesses is one of the most important tasks in managing any business. Accounting includes the preparation of financial reports and income statements, as well tracking expenses and income. You may also need to use software programs like Quickbooks Online. There are many options for accounting small businesses. You should choose the best way for you according to your needs. We have listed the best options for you below.

-

Use the paper accounting method. You may prefer paper accounting if you are looking for simplicity. This method is simple. You just need to keep track of your transactions each day. You might consider investing in an accounting software like QuickBooks Online if you want your records to be accurate and complete.

-

Use online accounting. Online accounting gives you the ability to easily access your accounts whenever and wherever you are. Wave Systems, Freshbooks, Xero, and Freshbooks are just a few of the popular options. These types of software allow you to manage your finances, pay bills, send invoices, generate reports, and much more. These programs offer many features and benefits. They also make it easy to use. So if you want to save time and money when it comes to accounting, you should definitely try out these programs.

-

Use cloud accounting. Another option is cloud accounting. It allows you to store your data securely on a remote server. Cloud accounting is a better option than traditional accounting systems. Cloud accounting isn't dependent on expensive software or hardware. Because all your information is stored remotely, it provides better security. Third, it saves you from worrying about backing up your data. Fourth, it makes it easier for you to share your files with other people.

-

Use bookkeeping software. Bookkeeping software is similar in function to cloud accounting. You will need to purchase a computer and then install the software. Once you have installed the software, the software will allow you to connect to the Internet so you can access your accounts whenever it suits you. You can also view your balances and accounts right from your computer.

-

Use spreadsheets. Spreadsheets are useful for entering financial transactions manually. For example, you can create a spreadsheet where you can enter your sales figures per day. Another benefit of using a spreadsheet is the ability to make changes at will without needing an entire update.

-

Use a cash book. A cashbook is a book that records every transaction you make. There are many sizes and shapes of cashbooks, depending on the space available. You can either use a separate notebook for each month or use a single notebook that spans multiple months.

-

Use a check register. You can use a check register as a tool to help you organize receipts or payments. Simply scan your items into your scanner to transfer them to the check register. Notes can be added to the items once they are scanned.

-

Use a journal. A journal is a logbook which keeps track of your expenses. This is a good option if you have lots of recurring expenses like rent and insurance.

-

Use a diary. A diary is simply a journal that you write to yourself. You can use it as a way to keep track and plan your spending habits.